{kind=link}

MVF Commences Distribution 9

December 2023 Update

MVF Distribution 9:

$158.9 million to 24,875 Madoff Victims

Victim recoveries reach 91% of fraud losses

► Victim recoveries brought to a minimum 91% of fraud losses

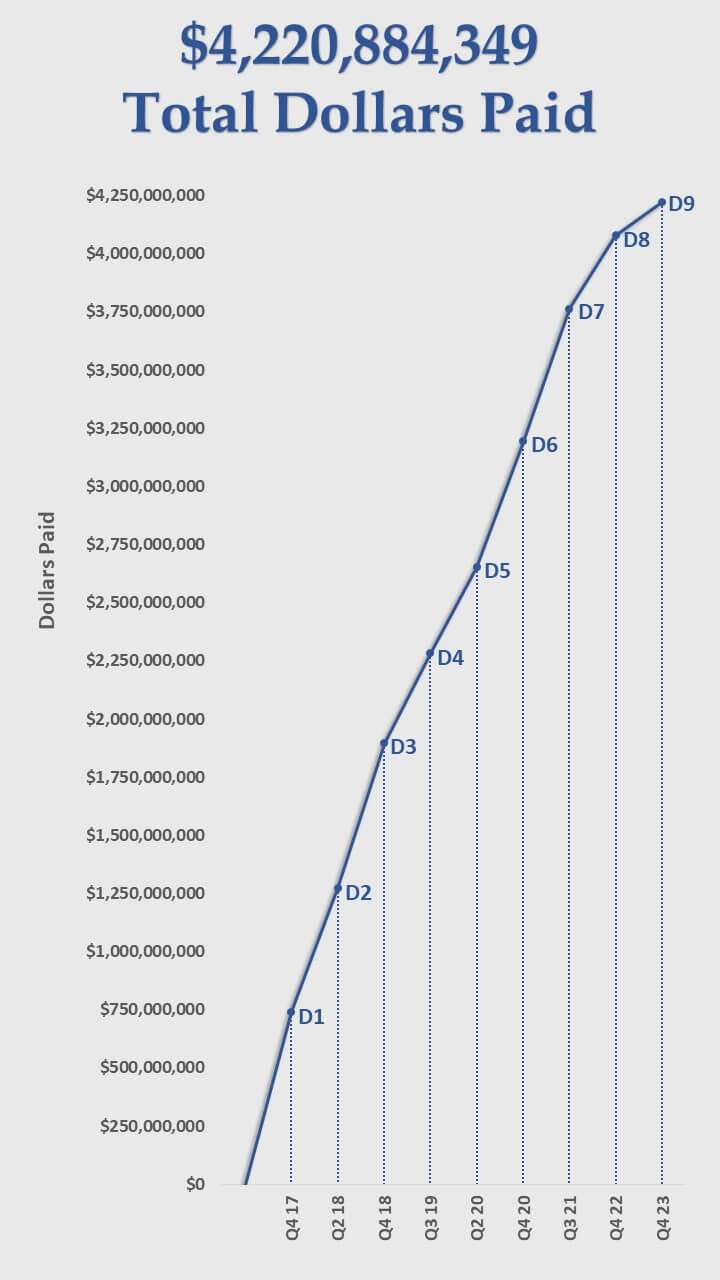

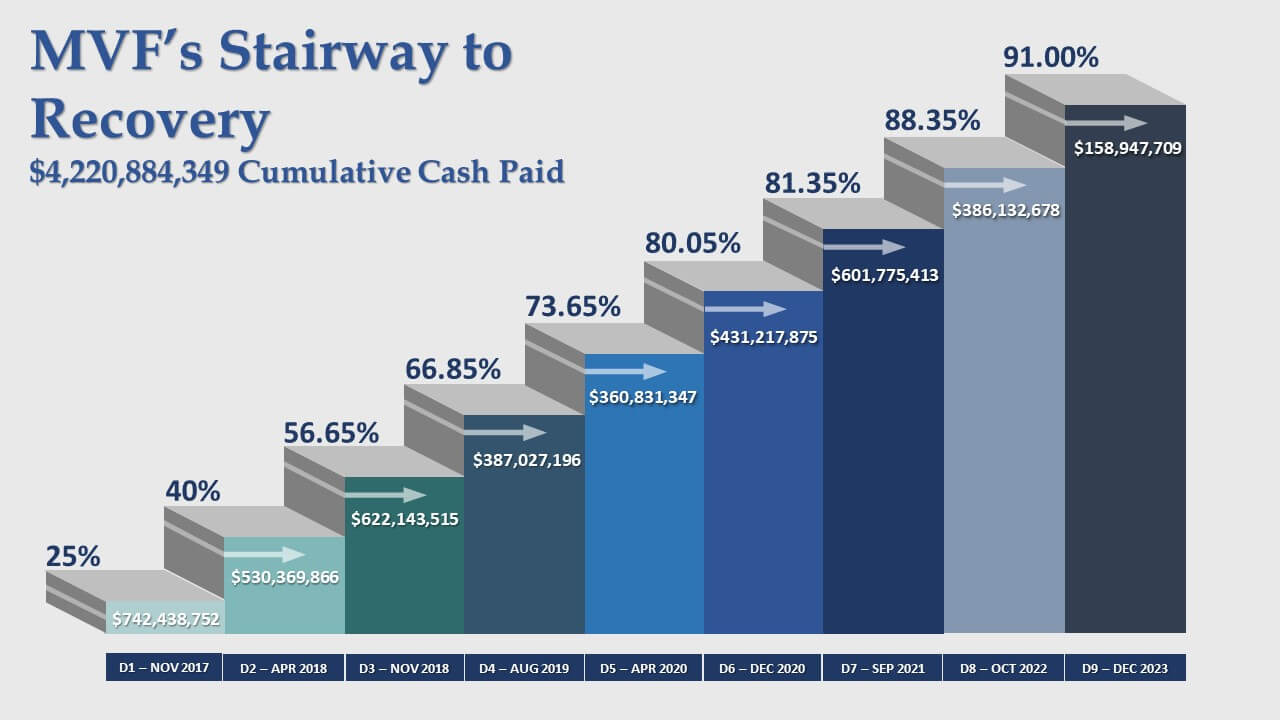

► In nine distributions, MVF has paid $4.221 billion directly to victims

► MVF has paid 40,843 petitioners in 127 countries

Special Master Richard C. Breeden of the Madoff Victim Fund made the following announcement:

91%!

“MVF was created by the Department of Justice ten years ago to identify everyone who was a victim of Madoff’s financial crimes, and to provide those victims with the highest possible recovery for their fraud losses measured in accordance with U.S. law. When we started, no one knew how many Madoff victims existed, where they were, or the amount of their losses. Now, in our tenth anniversary year, we have finally pushed past the 90% payout milestone.

MVF was created five years after discovery of the fraud and commencement of the Madoff bankruptcy. When our claim deadline passed in 2014, we realized that there were many thousands of victims who had not yet received meaningful compensation for their losses, and thousands more who had never received anything. The unaddressed losses of indirect investor victims were simply staggering.

MVF was created five years after discovery of the fraud and commencement of the Madoff bankruptcy. When our claim deadline passed in 2014, we realized that there were many thousands of victims who had not yet received meaningful compensation for their losses, and thousands more who had never received anything. The unaddressed losses of indirect investor victims were simply staggering.

Absolutely no one could have predicted that we would deliver total recoveries surpassing 90%. It has been a saga of endless hard work by people at MVF and the Department of Justice, all determined to change every crime victim’s life for the better. The Department did an amazing job recovering assets from people or entities that were involved with the fraud. We poured our collective energy and talents into delivering the greatest possible compensation and allocating funds to equalize recoveries among victims.

Today’s announcement is a realization of our dreams of what we could do to help so many people with shattered lives. At MVF, we have traced the contours of the fraud, calculated the stolen cash and then put it back directly into the hands of the people from whom it was stolen. Some thought that it wouldn’t be possible to document the cash lost by indirect investors given the complexity of the job. However, to paraphrase an old saying, our staff did the difficult right away, though the impossible took a bit longer.

My colleagues and I will forever be proud to have taken part in this monumental and unprecedented effort to restore the lives of so many victims. The Madoff crimes should not have passed without a relentless effort to overcome the suffering of victims, and to use recovered funds to assist every person whose money was actually stolen. MVF’s distributions help offset one of the most monstrous financial crimes ever committed. Nothing can make up for the lost years and trauma of victims, but at last we have been able to right this enormous wrong.”

Setting a New MVF Record for Total Payouts

In its ninth major distribution (“D9”), MVF is paying $158,947,709, or an additional 2.65% compensation on fraud loss to 24,875 eligible victims. This raises the percentage received by victims from our prior level of 88.35% to 91%. In all cases, this recovery level is computed after considering a victim’s recoveries from all sources. MVF has now provided cumulative payments of $4,220,884,349 to 40,843 victims of the Madoff fraud.

Because MVF payments go directly to the victim, the process is enormously efficient. For every $1 paid out by MVF, a victim actually receives $1. That is a ratio of 1:1 between payouts and victim receipts. The combination of forfeited funds available and the efficiency of the MVF process allowed us to provide a 91% recovery.

MVF’s total direct payments to 40,843 victims now exceed $4.220 billion.

Resolving Issues of “Collateral Recoveries”

DOJ regulations require MVF to reduce remission payments by amounts a victim has already received from other sources (“collateral recoveries”). Thus, MVF will not pay for “losses” that victims have already recovered. MVF’s reserves are finite, so double payments for some former Madoff investors would correspondingly reduce payments to all others. By bringing each victim to an equal percentage recovered from all sources, MVF prevents some victims from being overpaid, and others underpaid.

One goal of MVF was to level out the drastically different recovery percentages among different victims. Starting with D1 in November 2017 and continuing to D9, MVF set a series of percentage recovery baselines, shown in the chart below. In each distribution MVF brought every investor up to that level of recovery but did not pay anyone who had already recovered more than that from any source. This was particularly challenging in a limited number of cases where significant litigation contingencies existed.

One goal of MVF was to level out the drastically different recovery percentages among different victims. Starting with D1 in November 2017 and continuing to D9, MVF set a series of percentage recovery baselines, shown in the chart below. In each distribution MVF brought every investor up to that level of recovery but did not pay anyone who had already recovered more than that from any source. This was particularly challenging in a limited number of cases where significant litigation contingencies existed.

Reducing payments by the amounts of collateral recoveries is required by U.S. law applicable to remission. The purpose is to prevent some victims from receiving disproportionately large recoveries in comparison to others. Everyone who had their money stolen in the same crime should receive an equal level of recovery. Determining the amount of collateral recoveries for each of more than 42,700 eligible claimants has been an extensive task, particularly where assessments had to be made of likely future payouts. However, without this process overpayments to as many as 60% of all victims might have occurred.

Collateral Recovery Updates

By now, our petitioners understand the importance of MVF’s “collateral recovery update” (“CRU”) process. Under MVF’s payout process, we compute the amount necessary to bring each victim to the new recovery percentage threshold AFTER including all prior recoveries of the victim from any source. MVF cannot issue a check without up to date and accurate information on the petitioner’s recoveries from other sources. The update process is simple and allows MVF to calculate the correct payment amount for each victim prior to each distribution.

For D9, MVF set a deadline of October 15, 2023 for victims to submit a CRU. Fortunately, more than 23,000 persons with eligible claims have already submitted a CRU. MVF is still processing CRU submissions, and we hope to include every possible victim in the D9 distribution. However, petitioners eligible to receive a D9 payment who do not submit a CRU will not receive checks. MVF is still accepting late CRUs, and if you have not submitted a CRU for D9 please do so IMMEDIATELY! We don’t want anyone to miss participating, but we must know the amount of any changes in recoveries. You can easily satisfy the CRU obligation by clicking here or the button below.

Please remember, failing to update your collateral recoveries makes your original petition – filed under penalty of perjury – incomplete. Certifying falsely that you have not received recoveries or providing incomplete recovery information would be a violation of the law.

So, please be complete and accurate!

Update Your Collateral Recoveries

Collateral recovery updates are essential. Please use the website to update your MVF records so your payments are not suspended. Simply click the button below to begin.

Looking to the Future

At the outset of the MVF process we knew that we would be able to provide at least modest assistance to thousands of victims who were not eligible for recoveries from other sources. Even today nearly 10,000 victims eligible for a D9 check have received zero compensation from any source other than MVF. Altogether, more than 18,600 victims, or 75% of all victims eligible for D9 payments, have received less than 30% recoveries from other sources. These numbers highlight that MVF has been the lifeline for many victims, and we have reached far more people with far more dollars than originally anticipated. Achieving a 91% recovery, with a bit more to come, is well beyond what we thought we could achieve in the early days when MVF was formed.

We will continue to work hard through MVF’s remaining existence to push every victim’s recoveries higher than our current 91% level. At the same time, we will be reconciling every claim involving uncertainties during 2024. We anticipate making a final smaller distribution before the end of 2024.

Delivering payments of this magnitude directly to tens of thousands of victims has been very satisfying for everyone involved in the MVF process. We hope an effort of the scale of MVF’s is not needed again due to a future crime. However, if another such horrific event did happen, we hope that it will be handled with the same energy and relentless focus that the Department of Justice and MVF have brought to this case.

Respectfully,

Richard C. Breeden

Special Master, Madoff Victim Fund

Click here to view the Press Release from the U.S. Department of Justice announcing the ninth MVF distribution.

Click here to view the Press Release from The United States Attorney’s Office for the Southern District of New York.

► Case Update from the Special Master – Fall 2022

► Case Update from the Special Master – September 2021

► Case Update from the Special Master – December 2020

► Case Update from the Special Master – Spring 2020

► Case Update from the Special Master – Summer 2019

► Case Update from the Special Master – Fall 2018

Have questions about your claim? We’re here to help. U.S. based support, Monday thru Friday, 8:30am to 5pm EST.

1-866-624-3670

The Global Scope of Madoff’s Fraud

Claims Per Country as of December 2023

Letters from MVF Claimants Around the Globe

The Madoff Victim Fund strives to reach all the victims of the Madoff fraud. Send us a note if you would like to share your views.